Sebastian Heinermann (née Bleschke)

Managing Director

Contact:

+49 30 36418 086

info@energien-speichern.de

Foto:

studioline Photostudios GmbH

Reduced levels of gas production in the Netherlands force Germany to adapt its gas infrastructure. Five to six million customers have to switch from low-calorific L-gas to high-calorific H-gas. The transformation from L- to H-gas is already implemented. In 2017, INES has therefore produced a policy paper on the L-gas supply in Germany. It presents key facts and figures, identifies fields of actions, and points out possible solutions.

INES Policy Paper on L-Gas Supply (DE)Germany’s gas market consists of two different gas qualities: low-calorific L-gas and high-calorific H-gas. About five to six millions customers in the north and west of Germany currently use L-gas. Gas suppliers cooperate in the L-gas as well as in the H-gas area. However, physically these two gas qualities need to be separated. It has to be considered that each gas quality uses its own infrastructure – production, gas storage and pipelines.

Germany imports most of its L-gas from the Netherlands. A smaller share is produced from domestic gas fields. As the Dutch gas production ceases during the forthcoming decade and German production is decreasing, Germany has to adapt its infrastructure. It does so in a step-by-step process that lasts until 2030 transforming its L-gas facilities towards H-gas.

Considering this drastic transformation, the security of the L-gas supply is a valid concern. Increased L-gas imports and domestic production cannot ensure that enough L-gas is always available – especially during peak loads in the heating season.

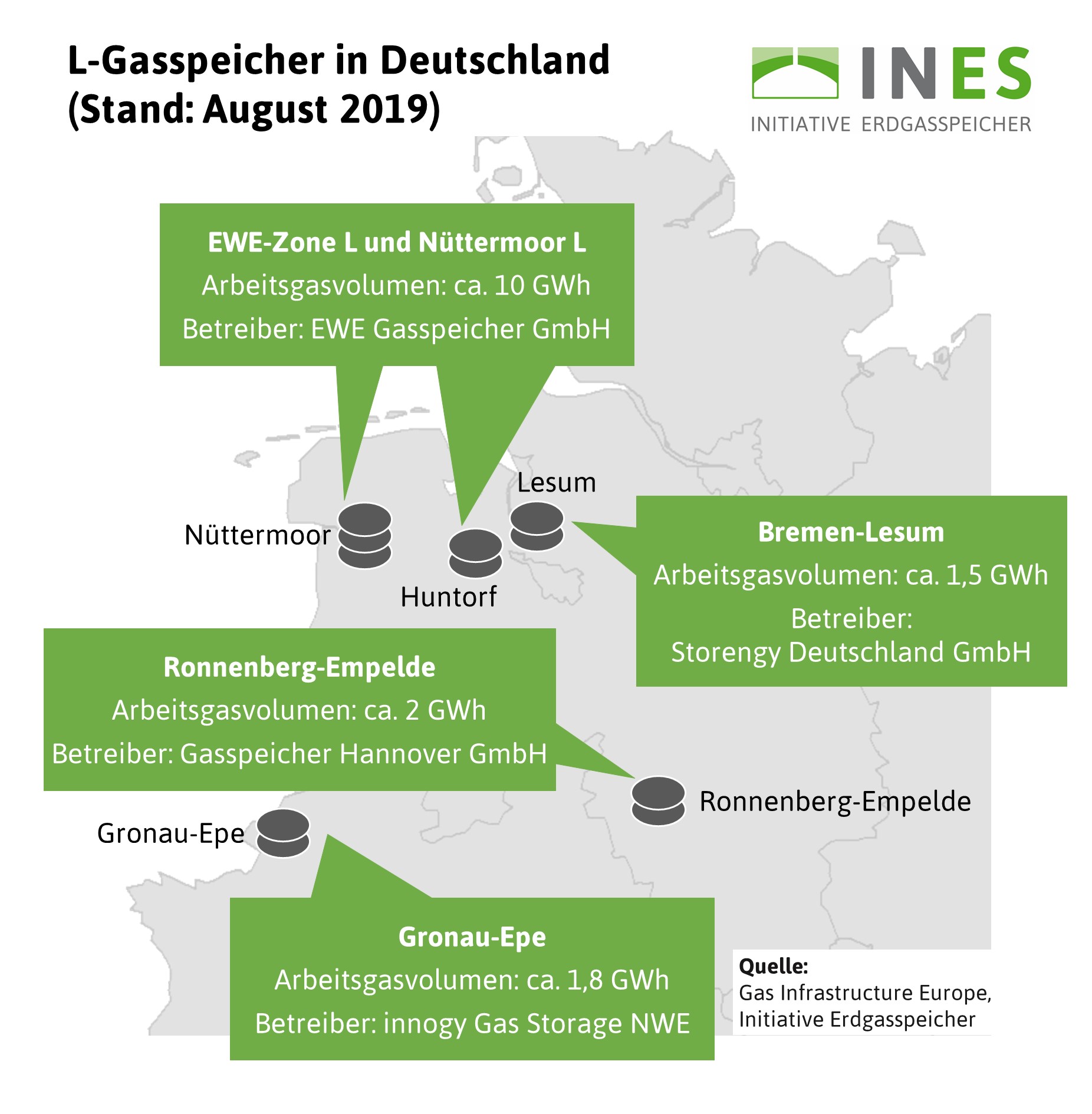

Providing an L-gas capacity of up to 33 gigawatt German gas storage in Empelde, Epe, Lesum, Nüttermoor and Huntorf therefore is a cornerstone of a secure L-gas supply. Gas storage facilities also avoid that pipelines are used below their capacity in times of a low gas demand as gas is injected here throughout the whole year. Gas storage thereby reduces transport costs for gas consumers.

Germany’s key instrument to develop competition between suppliers on the gas market are virtual trading points. On these trading points demand and supply in a certain market area are supposed to be balanced. In Germany there are two market areas at the moment: NetConnect Germany and Gaspool. From October 2021 there will only be one market area left in Germany.

Key participants in the gas market are balancing group managers. Balancing group managers are responsible that gas demand and gas suppy in a certain area are levelled. Next to delivering actual L-gas to customers, the balancing group managers can also use H-gas on the virtual trading point to balance their group. That means they can choose to take H-gas to trade or deliver L-gas to their L-gas customers.

As L-gas consumers cannot actually receive H-gas, the Market Area Coordinators Netconnect Germany and Gaspool fulfill a special role in the market. Both companies have to take technical or commercial measures in order to secure a physically balanced gas pipeline grid.

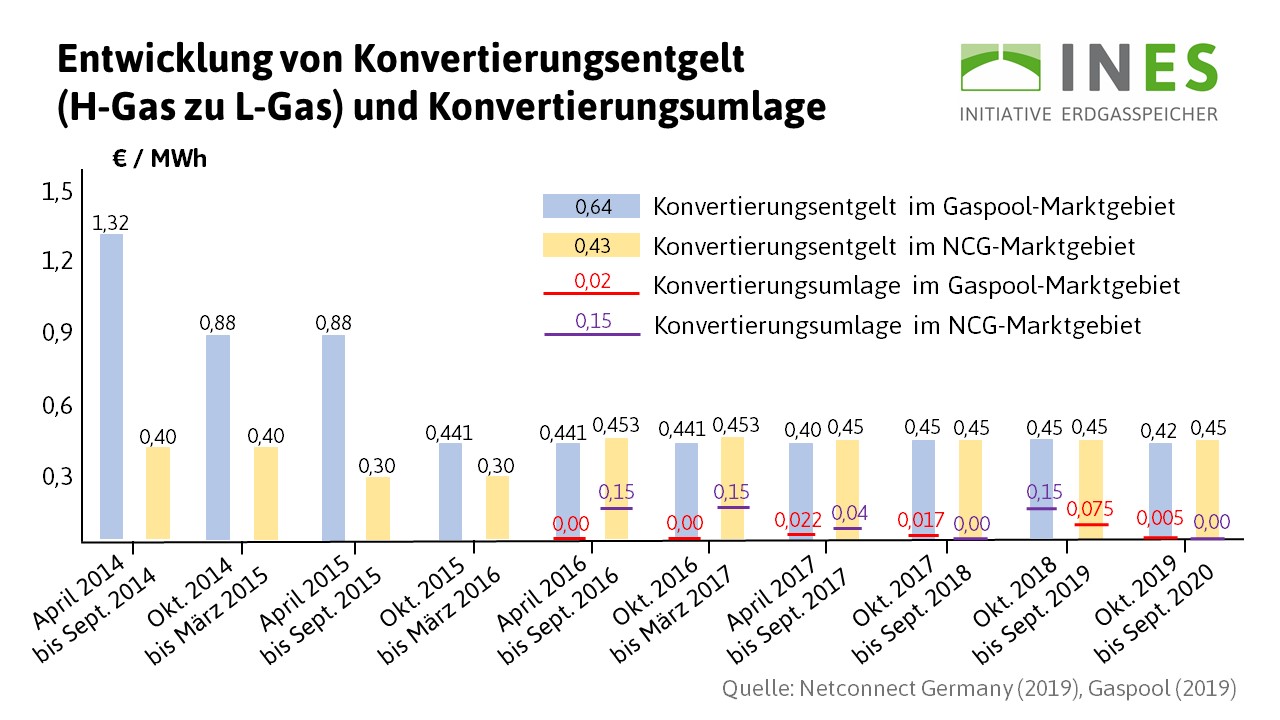

The price of this service is paid by consumers through a conversion tariff (the so-called Konvertierungsentgelt). If conversion costs surpass the gains from the conversion tariff, the Market Area Coordinator can charge an additional conversion levy (the so-called Konvertierungsumlage).

Another levy in the gas market is the market transition levy (so-called Marktraumumstellungsumlage). That levy socializes costs that Grid Operators carry because of technical measures to ensure the transition from L-gas to H-gas. That means the levy is paid by all consumers using exit capacities from German long-distance pipeline networks.

Sebastian Heinermann (née Bleschke)

Managing Director

Contact:

+49 30 36418 086

info@energien-speichern.de

Foto:

studioline Photostudios GmbH